Reagan’s Advisor: Trump’s Trade War is Crippling Dollar Hegemony

The Truth Behind the U.S. Trade Deficit

The China Academy: In a previous podcast, you mentioned your opposition to protectionism and your belief that trade is not a zero-sum game. You also argued that the U.S. trade deficit does not mean the U.S. is losing, and that viewing U.S.-China trade relations through such a lens is misguided. Through what lens, then, should we view U.S.-China trade relations?

Steve Hanke: Let me start with the concept of a zero-sum game. A zero-sum game is really a mercantilist idea that has been around since the 15th and 16th centuries. Mercantilists believed that whenever a country had a trade surplus, another country must be incurring a trade deficit of the exact same amount. Therefore, trade was seen as a zero-sum game, where one side’s benefit was offset by the other side’s loss.

The mercantilists always wanted to have a positive trade surplus, essentially exporting more than they imported. That was their central idea, and unfortunately, most people still think this way today—not just in America, but also in China, Indonesia, and Europe. This is what the average person believes.

The reason for this misunderstanding, I think, is that businesses operate based on a profit and loss system. People see revenue coming in as a positive and costs going out as a negative. Businesses aim for revenue to exceed costs to make a profit, and people assume that a country’s trade is the same as operating a business. This is what economists call the fallacy of composition. The fallacy occurs when people take an idea that applies to an individual (like a business) and mistakenly scale it up to apply to an entire country.

But trade is clearly not a zero-sum game. Let me give you an example. Imagine you’re selling me something, and we agree on the terms, including the price. This means you benefit because you agreed to sell the item—if you didn’t think it was a good deal, you wouldn’t sell it. On the other hand, I, the buyer, also think it’s a good deal, or I wouldn’t buy it. Both of us gain from the transaction. You’re not gaining at my expense, and I’m not losing because I paid you something. This is where mercantilist thinking goes wrong.

So, the fallacy of composition and the idea of a zero-sum game are flawed. What actually creates trade imbalances? That’s what we need to understand.

To explain this, I recommend an article I co-authored with Edward Li titled The Strange and Futile World of Trade Wars. In the article, we explore the standard identity in economics, which states that savings equal investment. If savings are less than investment in an economy, it will have a trade deficit equal to that difference. Conversely, if savings exceed investment, the economy will have a trade surplus.

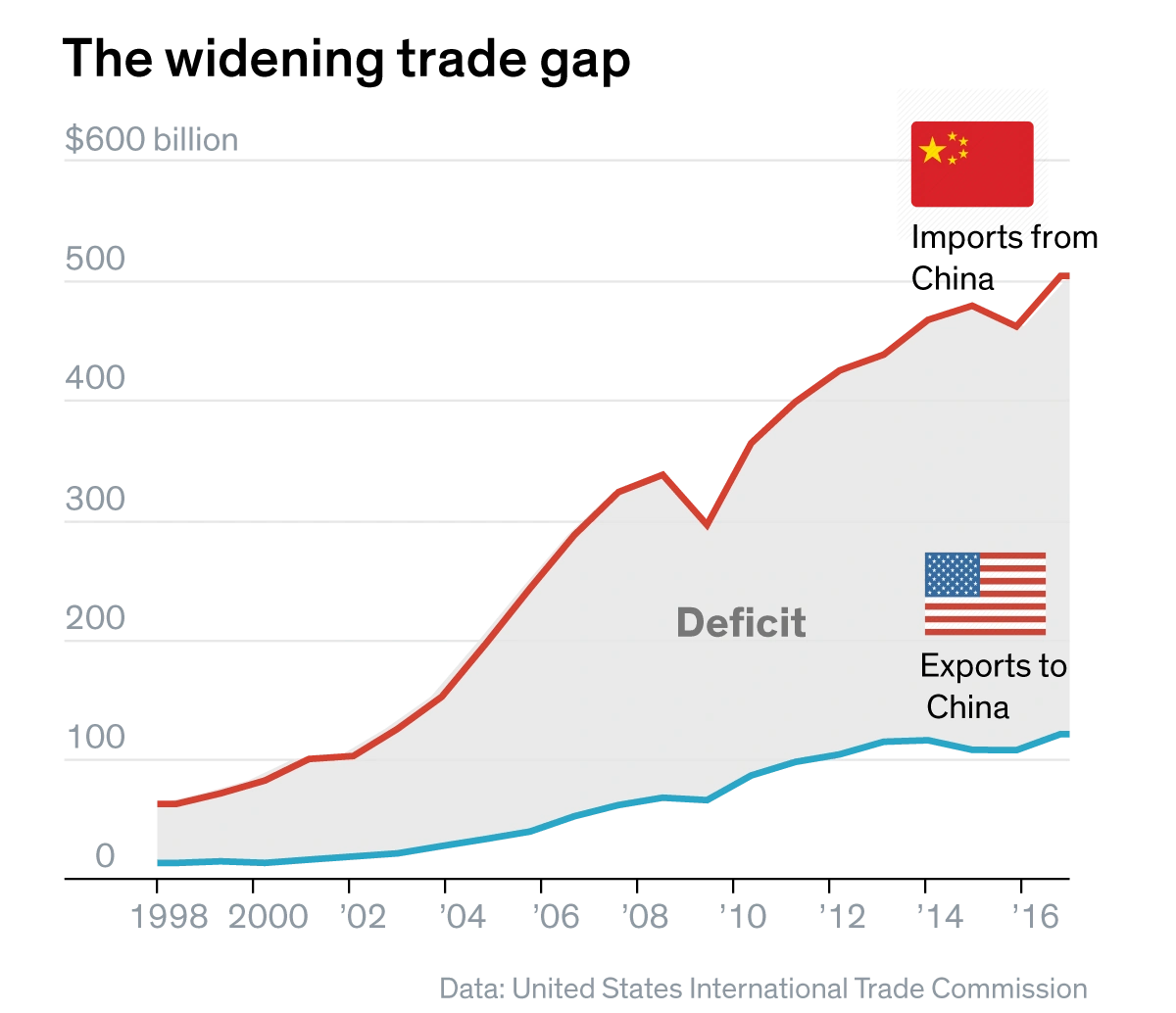

So, why does China have a huge trade surplus? It has nothing to do with exchange rates, trade policies, or the usual factors discussed in the media. It’s simply because the Chinese save far more than they invest. This is the same reason Switzerland consistently has a trade surplus—because the Swiss save more than they invest. Similarly, Germany typically has trade surpluses because Germans save more than they invest.

Now, what about the United States? Since 1975, the U.S. has run a trade deficit every single year. The reason for this is that the U.S. has a savings deficiency—the amount of savings in the U.S. is much less than the amount of investment.

In our article, Edward Li and I did something that had never been done before: we analyzed the data, looking at both private and public sector savings and investments. This included savings and investments at the federal, state, and local government levels.

What we found was striking. The private sector in the U.S. actually has a surplus of savings. However, the public sector runs a huge deficit in savings, and this deficit is about twice the size of the private sector’s savings surplus. When you combine these, the result is a net savings deficiency, which explains why the U.S. has a trade deficit.

Now, is this a problem? Not at all.

The U.S. can easily finance its trade deficits by borrowing at low interest rates because the U.S. dollar is the world’s dominant currency. The U.S. has been doing this for decades, and it works well. The trade deficit allows Americans to consume far more than they produce, with the gap being filled by imports. This is a good deal for U.S. consumers, who enjoy a high standard of living.

If the U.S. wanted to eliminate the trade deficit—though this wouldn’t be a good idea—the easiest way would be to balance the public sector budget. Without the public sector deficit, the savings deficiency would disappear, and the trade deficit would go away. In short, the fiscal deficit at the federal, state, and local levels is the main driver of the U.S. trade deficit. In this sense, it’s the government that causes the trade deficit by running large fiscal deficits.

This is a key lesson about trade that most people don’t understand. They don’t realize that the federal deficit is the main reason for the trade deficit. They also mistakenly believe that trade deficits are inherently bad. But if a trade deficit is easily financed, it can actually be beneficial.

Now, let’s turn back to China. Many economists argue that China needs to start consuming more and saving less. If that happens, China’s trade surplus would naturally decline. People also misunderstand China’s trade surplus, often claiming that it comes from overcapacity and flooding other countries with excess production. But that’s not the case. The real reason for China’s trade surplus is its high savings rate, which creates a surplus of savings. According to economic identities, this surplus necessarily translates into a trade surplus.

Trump’s Trade War on China

The China Academy: How do you evaluate Trump’s much-touted trade war?

Steve Hanke: First of all, I think high-tariff policies—or protectionist policies in general—are completely misguided. I’m totally against them.

Back in the early 1980s, I was one of President Reagan’s advisors. During my time at the President’s Council of Economic Advisers, as well as working with the U.S. Treasury and the Office of Management and Budget, my stance was clear: I was—and still am—a free trader. Reagan was also a free trader. This means we opposed tariffs, quotas, sanctions, and any kind of interference in trade.

Trade is a mutually beneficial activity. That’s why I’m a unilateral free trader—I believe in no trade restrictions whatsoever.

From the U.S. perspective, I think the policies we’ve adopted in recent years, including tariffs, quotas, and sanctions, have been very damaging. Not only do they hurt the countries or firms being targeted, but they also harm the United States.

Now, let’s talk about Trump. Trump is not a free trader—he’s a mercantilist. He believes that trade is a zero-sum game, where one side’s gain is equal to the other side’s loss. For example, he thinks restricting imports benefits the U.S. while imposing an equal cost on the exporting country, such as China.

This kind of thinking is not new. Back in the early 1980s, the U.S. was dealing with a massive trade deficit, but the “enemy” at that time wasn’t China—it was Japan. Tremendous amounts of imports were coming from Japan into the U.S., and there was significant political pressure on President Reagan to impose trade restrictions. Reagan, despite being a free trader, had to navigate this pressure from Congress, other politicians, and even some members of his administration, like Malcolm Baldrige, the Secretary of Commerce, who supported protectionist measures.

As a result, Reagan’s administration implemented more trade restrictions than any U.S. administration since Herbert Hoover.

Now, fast forward to Trump. Unlike Reagan, Trump fully embraces mercantilist ideas. He views tariffs and quotas as tools to benefit the U.S. while imposing costs on other countries. He also sees them as a kind of “club” to pressure other nations. For example, he’s used the threat of tariffs in discussions with Mexico and Canada. Just recently, he met with Canadian Prime Minister Justin Trudeau, who expressed concerns about these tactics.

Economically, using tariffs as a weapon is a bad idea. Diplomatically, it’s even worse. This is not how you build alliances or foster cooperation. If Trump goes to China to meet Chairman Xi and says, “Do what I want, or I’ll impose tariffs on you,” it’s not an effective diplomatic strategy. It will lead to counterattacks because tariffs are essentially a declaration of a trade war.

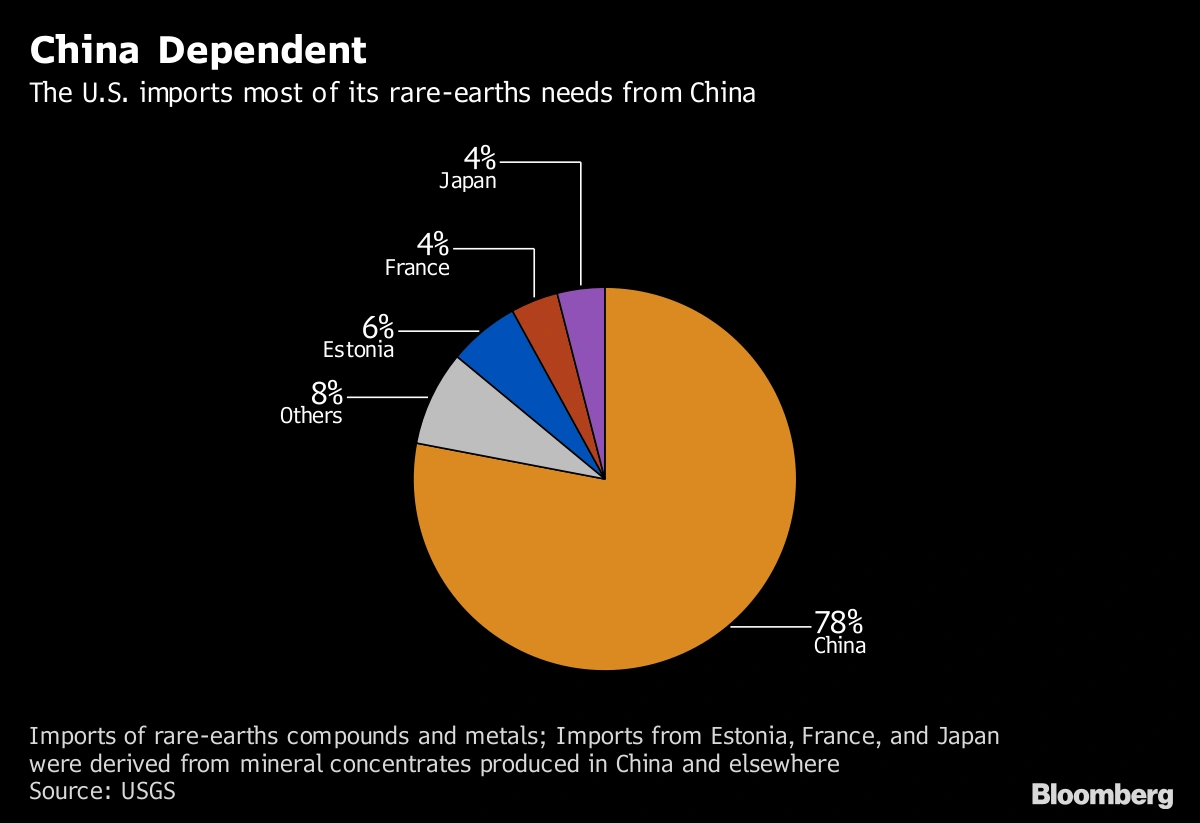

China, by the way, is prepared for such a trade war. They have plenty of ammunition, including their control over rare earths, critical materials, and other resources that are essential for global industries.

If China retaliates, it will hurt the U.S., but it will also hurt China. Trade wars are not a zero-sum game or even a positive-sum game. They are a negative-sum game, where both sides lose.

The China Academy: Building on the importance of rare earths and other critical materials, I read in one of your articles that China is responsible for 90% of the production of rare earth magnets and has taken control of various other critical materials essential for the global transition to a green economy. How will this aspect factor into China’s competition with the U.S. and its own economic transition?

Steve Hanke: I call it the “three M’s”: mining, metallurgy, and material science. These are the key areas to focus on when evaluating this competition.

China dominates these fields, and one way to understand this is by looking at university education and training in the three M’s. Globally, if you examine the top 20 universities overall, none of them are in China. But when you narrow the focus to specific fields, such as mining, 14 of the top 20 universities are in China. Similarly, in metallurgy, 14 of the top 20 universities are also in China. For material science, the number drops slightly, but still, 6 out of the top 20 universities are in China.

This clearly shows that China leads in knowledge and expertise in mining, metallurgy, and material science. Many people mistakenly think rare earths are just resources in the ground that you dig up. But extracting and processing rare earths requires extremely complex chemical processes. In these areas, China is far ahead of any other country.

The Chinese have been aware of the importance of these critical materials for a long time. Deng Xiaoping famously said, “The Middle East has oil, China has rare earth metals.” This highlights China’s strategic understanding of the significance of rare earths and other critical materials.

If China wanted to counterattack in a trade or economic conflict, they could leverage their dominance in rare earths and other critical materials by cutting off supplies. Such an action would be highly disruptive to the global economy, especially in the transition to green energy, where these materials are essential.

How Money Supply Influences the U.S. Economy and Election Outcomes

The China Academy: You successfully predicted Trump’s victory and attributed it largely to the Federal Reserve’s policies under the Biden administration, which widened wealth inequality. Could you elaborate on your argument that the money supply is the root cause and that the U.S. economy is heading for a recession in 2025?

Steve Hanke: This question gets to the heart of monetary policy and its transmission mechanism. To understand this, we need a model for what we call national income determination. National income, or nominal GDP, consists of two components: real output (real GDP) and inflation. If you add real economic growth to inflation, you get nominal GDP.

The most reliable model for predicting nominal GDP is based on the quantity theory of money. Money is the fuel of the economy—if you increase the money supply, nominal GDP rises. The transmission mechanism works as follows:

When the money supply changes, the first effect (with a lag) is on asset prices. For example, if the money supply increases significantly, the prices of assets—such as stocks, real estate, land, and automobiles—go up.

With a further lag, the real economy begins to respond, either accelerating or decelerating depending on whether the money supply is expanding or contracting. This affects real GDP.

Finally, the last impact is on inflation, which rises or falls depending on the money supply changes.

Now, let’s look at what happened in the U.S. during COVID-19. In early 2020, when the pandemic hit, the Federal Reserve dramatically increased the money supply. As a result, asset prices soared—real estate, land, and the stock market all experienced huge increases.

But here’s the key: who owns assets? Wealthy people do. Poor people, on the other hand, typically don’t own homes, cars, or stocks. For example, I recently calculated that in February 2020, just before COVID hit, the collective wealth of U.S. billionaires was 14.2% of GDP. As of today, that figure has ballooned to 21.2% of GDP. Billionaires, who were already rich, became super-rich due to this massive money supply expansion.

Meanwhile, the “little guy” suffered. Most lower-income individuals don’t own assets. Their incomes remained stagnant, but inflation rose, meaning their real (inflation-adjusted) incomes fell. This disparity created significant resentment among lower-income voters. They intuitively understood that the rich were getting richer while they were falling further behind. I believe this resentment was a key factor in the election outcome.

Now, let’s look at the current situation. Since July 2022, the U.S. money supply, as measured by M2, has been contracting. This has only happened four times since the Federal Reserve was established in 1913, and each time it was followed by a recession. When the money supply contracts, the economy slows down, and inflation falls. That’s why I believe the U.S. economy is headed for a recession in 2025, and inflation will continue to decline.

This also ties into what’s happening in China. As a monetary economist, I find China’s current stimulus program very interesting, but I don’t think it will work. Why? Because the money supply in China isn’t growing fast enough to support the economy or hit the government’s inflation target of 3%.

To meet that target, China’s money supply (M2) would need to grow at what I call “Hanke’s golden growth rate”—about 11% per year. Right now, it’s only growing at 7.4–7.5% year-over-year. That’s far too slow. Without sufficient money supply growth, the economy lacks the necessary fuel to stimulate real growth.

Let me give you some historical context. During the 2008 global financial crisis, China did exactly the right thing. In November 2008, China’s money supply was growing at 15% per year. By November 2009, it was growing at 30% per year—a massive acceleration.

What happened as a result? Let’s look at the transmission mechanism:

In July 2009, China’s Consumer Price Index (CPI) was negative (-1.8%), indicating deflation. By July 2011, inflation had surged to 6.5%.

Real GDP growth also accelerated: in Q4 2008, it was 7.1%; by Q4 2009, it had jumped to 11.9%, and by Q4 2010, it was 9.9%.

In other words, China increased the money supply dramatically, and this fueled both real growth and inflation, pulling the economy out of deflation and stimulating rapid expansion.

Right now, China faces the opposite problem. Its money supply is growing too slowly. Inflation is almost nonexistent—just 0.2% per year—far below the 3% target. The only way to raise inflation and stimulate the economy is to increase the money supply.

Unfortunately, unless China accelerates its money supply growth, the current stimulus program will fail. History provides a clear example of what worked during the 2008 financial crisis, but those lessons are not being applied today. Without sufficient money supply growth, the Chinese economy will remain stagnant, and inflation will continue to stay far below target.

Trump’s Deep-Seated Fear of De-Dollarization

The China Academy: We read the latest news that Trump is threatening a 100% tariff on BRICS nations if they attempt to replace the U.S. dollar. Why is Trump so nervous about de-dollarization?

Steve Hanke: This is an interesting topic. First, it’s important to understand that there’s always one dominant international currency, and right now, that is the U.S. dollar. Historically, it’s very hard to dethrone the “king.” If we look back over the past 2,000 years, there have only been 14 dominant international currencies, and at any given time, there’s only one. The U.S. dollar is currently that dominant currency, and it’s not easy to knock it off the throne.

However, the U.S. is making some very poor decisions, particularly by weaponizing the dollar. For example, the U.S. has imposed sanctions on Russia, Iran, and anyone else they don’t like. One of the ways sanctions work is by cutting sanctioned parties off from the U.S. dollar system. In this way, the U.S. uses the dollar as a weapon. I think this is a bad policy—it’s unwise and short-sighted.

Despite these poor decisions, the dollar is likely to remain the global king. It’s incredibly difficult to replace a dominant currency, as history has shown. Out of the 14 dominant currencies we’ve seen over the last 2,000 years, changes are rare and often take significant upheaval.

Now, let’s talk about Trump. Trump’s stance on the dollar is inconsistent and contradictory. On one hand, he is pro-dollar. He wants everyone to keep using the dollar, and he’s even threatening BRICS nations with tariffs if they try to replace it. He’s wielding his usual “tariff club” to intimidate them into maintaining the dollar’s dominance.

On the other hand, Trump’s actions are also negative for the dollar. He supports the continued weaponization of the dollar through sanctions and has even suggested increasing sanctions on countries like Iran. This makes the dollar less attractive as a global reserve currency. Additionally, Trump is pro-cryptocurrency, which is another factor that undermines the dollar.

So, we see a contradiction: Trump pushes policies that support the dollar’s dominance, while simultaneously promoting actions that weaken it. Many of his economic ideas lack consistency.

To summarize, I’m against the weaponization of the dollar. It’s a bad policy, and it creates unnecessary risks for the U.S. But the claims that the dollar is on the brink of collapse are simply not correct. The dollar dominates and will continue to dominate for the foreseeable future.

Weaponization of the U.S. Dollar

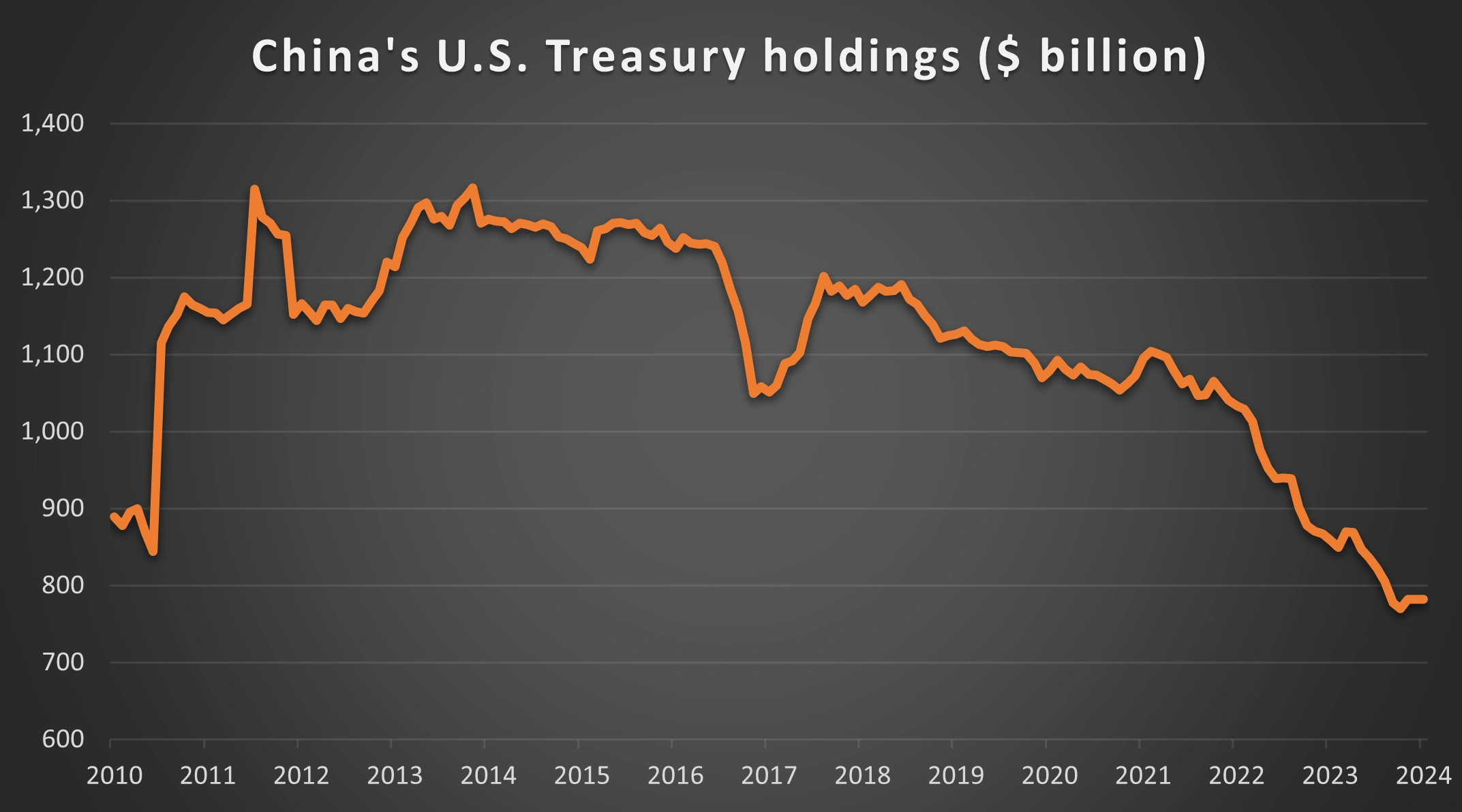

The China Academy: We’ve noticed that China and Japan have been reducing their holdings of U.S. Treasury bonds in recent years. What’s your view on this trend?

Steve Hanke: To some extent, this reflects the risks introduced by the U.S.’s weaponization of the dollar. When the U.S. imposes sanctions and uses the dollar as a tool to punish other countries, it makes foreign governments uneasy about holding U.S. Treasury bonds. If the U.S. wasn’t threatening or sanctioning other nations, I believe China and Japan wouldn’t be reducing their holdings of U.S. debt.

This is why weaponizing the dollar is such a bad policy from the U.S. perspective. When you weaponize the dollar, you also weaponize anything denominated in dollars—like U.S. Treasury bonds. This creates anxiety among foreign holders of U.S. debt, who may start to view it as risky.

For example, China may reduce its holdings of U.S. Treasury bonds not because of purely financial reasons, but for strategic or political reasons. They may be thinking, “What might the U.S. do to us next?” The uncertainty makes them less willing to hold U.S. bonds.

Additionally, the weaponization of the dollar increases the risk premium on U.S. Treasury bonds. Foreign holders now demand slightly higher interest rates because of the perceived risk. If the U.S. weren’t weaponizing the dollar, these bonds would likely be more attractive and could even be sold at lower interest rates.

However, there’s also a broader issue: the U.S. federal deficit and debt. These are unsustainable. As I often say, if something isn’t sustainable, it will eventually stop. The U.S. will have to address its deficit and debt problem sooner or later.

There are only three ways to fix this:

Reduce government spending – The U.S. would need to significantly scale back its expenditures.

Increase taxes – This could include direct taxes or other forms of revenue generation.

Inflation tax – The government could allow inflation to erode the real value of its debt.

In reality, it’s likely to be some combination of these three approaches. But until the U.S. addresses its unsustainable fiscal trajectory, the risks associated with its debt will remain, and foreign holders—like China and Japan—will continue to reduce their exposure.

Trump’s Department of Government Efficiency

The China Academy: In your podcast, you discussed the upcoming Department of Government Efficiency under the leadership of Elon Musk, noting that it could be a challenging task, especially since President Reagan attempted a similar effort in the past but failed. Could you elaborate on the reasons for your concern?

Steve Hanke: Musk and Ramaswamy are the two personalities who will be leading this so-called “Department of Government Efficiency.” But let me point out something: the very name of this department is a bit of a contradiction, because governments, by their nature, are not efficient.

Why aren’t they efficient? It comes down to incentives. A civil servant doesn’t operate under the same incentives as someone in the private sector who works within a profit-and-loss system. In government, you don’t get efficiency. Instead, you get waste, fraud, and abuse.

Let me give you some historical context. In 1982, President Reagan formed something called the Grace Commission, led by Peter Grace, the chairman of W.R. Grace & Co., a large conglomerate. Grace was a smart and capable leader, and he assembled a team of experts, including myself, as I was part of Reagan’s Council of Economic Advisers. In 1984, the Grace Commission issued its final report, which contained 2,500 recommendations for reducing waste and making the government more efficient.

But here’s the catch: almost none of those recommendations were implemented. This is why I’m skeptical about Musk and Ramaswamy’s chances of success. Of course, if they manage to reduce regulations or shrink the government, that would be great. But my experience, and my understanding of how government works, makes me doubtful.

To give you some further background, I worked directly on Reagan’s privatization initiatives. In fact, the word “privatization” itself has an interesting history. It’s a French word—privatisation—and my wife, who is French, introduced me to it. In 1981, I gave a speech in Reno, Nevada, where I used the term “privatization” for the first time in the English language. We even got the word into Webster’s Dictionary by 1983.

Reagan’s administration had plans to privatize surplus assets in the U.S., including the vast amounts of federal land in the western states—land that accounts for nearly 25% of the country’s total area. This land, used for grazing and timber, was owned by the federal government but was poorly managed. Reagan included the privatization of these lands in his 1983 fiscal budget, and I personally wrote the paragraph proposing this in the budget introduction.

But guess what? It never happened. There was too much political resistance—both locally and nationally. Similar resistance is what Musk and Ramaswamy will face. Civil servants will resist being fired, losing their pensions, or having their departments downsized. The political hurdles are enormous.

Here’s the problem: businessmen often think they can manage the public sector like they manage a business, but the public sector operates under completely different rules. For example, if something isn’t working at Tesla, Musk can fire employees or eliminate entire departments. But you can’t do that in the public sector. The politics are far more complicated, and the rules make it nearly impossible to apply private-sector methods.

Take military bases, for instance. The U.S. Defense Department has many surplus military bases that are no longer needed. But every state—there are 50 in total—has military bases. If you try to shut one of these down, you’ll face opposition from two U.S. senators and at least one congressman from that state. These politicians will resist because they don’t want to lose jobs or federal funding tied to the base, even if the base is completely unnecessary.

I’ll give you another ridiculous example. In the early 1980s, I discovered that the Defense Department had warehouses full of vacuum tubes—the kind used in old radios before transistors and microchips were invented. These vacuum tubes were completely obsolete by then, but when I suggested getting rid of them, they resisted. Their reasoning? “You never know—we might need them someday.” They also argued that since they weren’t paying rent for the warehouses and had already purchased the tubes, there was no harm in keeping them. In the end, we couldn’t even get rid of the vacuum tubes.

So when I hear about Musk and Ramaswamy leading a “Department of Government Efficiency,” I can’t help but be skeptical. The challenges they will face are deeply rooted in the structure and incentives of government, and those are very difficult to change.

The Challenges of revitalizing U.S. Manufacturing

The China Academy: Trump has stated that he intends to revitalize U.S. manufacturing during his term. From an economist’s perspective, what are your expectations for this goal?

Steve Hanke: The idea of “revitalizing manufacturing” has always been a political talking point. But what does that actually mean? If we look at the numbers, manufacturing output in the United States has been steadily increasing. So, in terms of output, there’s nothing to revitalize—it’s already growing.

What’s actually been declining is the number of manufacturing jobs. This is because productivity in manufacturing has been increasing. As automation, robotics, and artificial intelligence (AI) become more prevalent, manufacturing requires fewer workers to produce more output. This is the trend: higher productivity, more automation, and fewer jobs.

When politicians talk about revitalizing manufacturing, they often mean creating more manufacturing jobs. But that’s simply not going to happen. The reality is that automation and AI are job destroyers in certain sectors. Robots replace workers; AI replaces routine tasks.

However, while automation and AI destroy certain jobs, they also create opportunities in other areas. They shift the workforce toward different kinds of jobs. This is a natural process in advanced economies. But the idea that we’ll see a massive increase in manufacturing jobs in the U.S. is a pipe dream.

This trend is not unique to the United States. It’s the same in Europe and other advanced economies. Manufacturing output continues to rise, but employment in the sector declines due to innovation and increased productivity.

Now let me address AI specifically. There’s a lot of hype surrounding AI. For example, some people in Silicon Valley claim that AI could increase the U.S. real growth rate to 6% per year or more. That’s nonsense. The potential real growth rate of the U.S. economy is about 2.2%, and AI isn’t going to change that dramatically.

AI will have an impact in specific sectors, but it’s important to keep things in perspective. Only about 5% of U.S. jobs are directly exposed to being significantly affected by AI. These jobs tend to involve routine, repetitive tasks. So while AI is important, its overall effect on the labor force is limited compared to the hype.

In conclusion, while automation and AI are driving changes in the economy—some positive and some disruptive—revitalizing U.S. manufacturing by creating more jobs is not realistic. The focus should instead be on adapting to these changes, retraining workers, and fostering innovation in other sectors.

New book:Capital, Interest, and Waiting

The China Academy: My last question is about your new book, Capital, Interest, and Waiting. It seems to challenge some traditional economic ideas. What are the key conventional views that you sought to challenge in this book?

Steve Hanke: This book is essentially a treatise on capital theory, which is a crucial area of economics. Capital theory is important because the stock and quality of capital are major factors that determine an economy’s potential growth rate.

If an economy has no capital, it cannot grow. Conversely, if an economy has a large stock of high-quality capital, its potential growth rate will be much higher. But how do you accumulate capital? This happens through waiting—and waiting carries a cost, which is reflected in the interest rate.

Now, let’s define “waiting.” A unit of waiting occurs when you defer one unit of consumption for one unit of time. In other words, instead of consuming everything today, you choose to wait. But waiting isn’t free—you need to be compensated for delaying consumption. That compensation is the interest rate. Without it, people would consume everything immediately, and no capital would accumulate.

Here’s where our book challenges the conventional view. Traditional economic textbooks argue that there are three inputs into the production process: land, labor, and capital. The idea is that combining these three inputs leads to economic output.

But in our book, Professor Yeager and I argue that this framework is incorrect. We show that the true inputs into the production process are land, labor, and waiting. Capital, in fact, is just the embodiment of land, labor, and waiting. This changes the way we analyze economic growth and interest rates.

For example, waiting—saving and investing rather than consuming everything immediately—creates the stock of capital that fuels growth. The interest rate, as the price of waiting, plays a central role in determining the supply and demand for waiting. This, in turn, influences how much capital is accumulated and how fast the economy can grow.

To summarize, our book reframes the way we think about economic growth, interest rates, and capital. By recognizing that waiting, not capital, is one of the fundamental inputs into the economy, we offer a clearer framework for understanding how growth happens and how interest rates function.

Editor: huyueyue