The post China Will In No Way Repeat U.S. and Japan’s Real Estate Crises first appeared on China Academy.

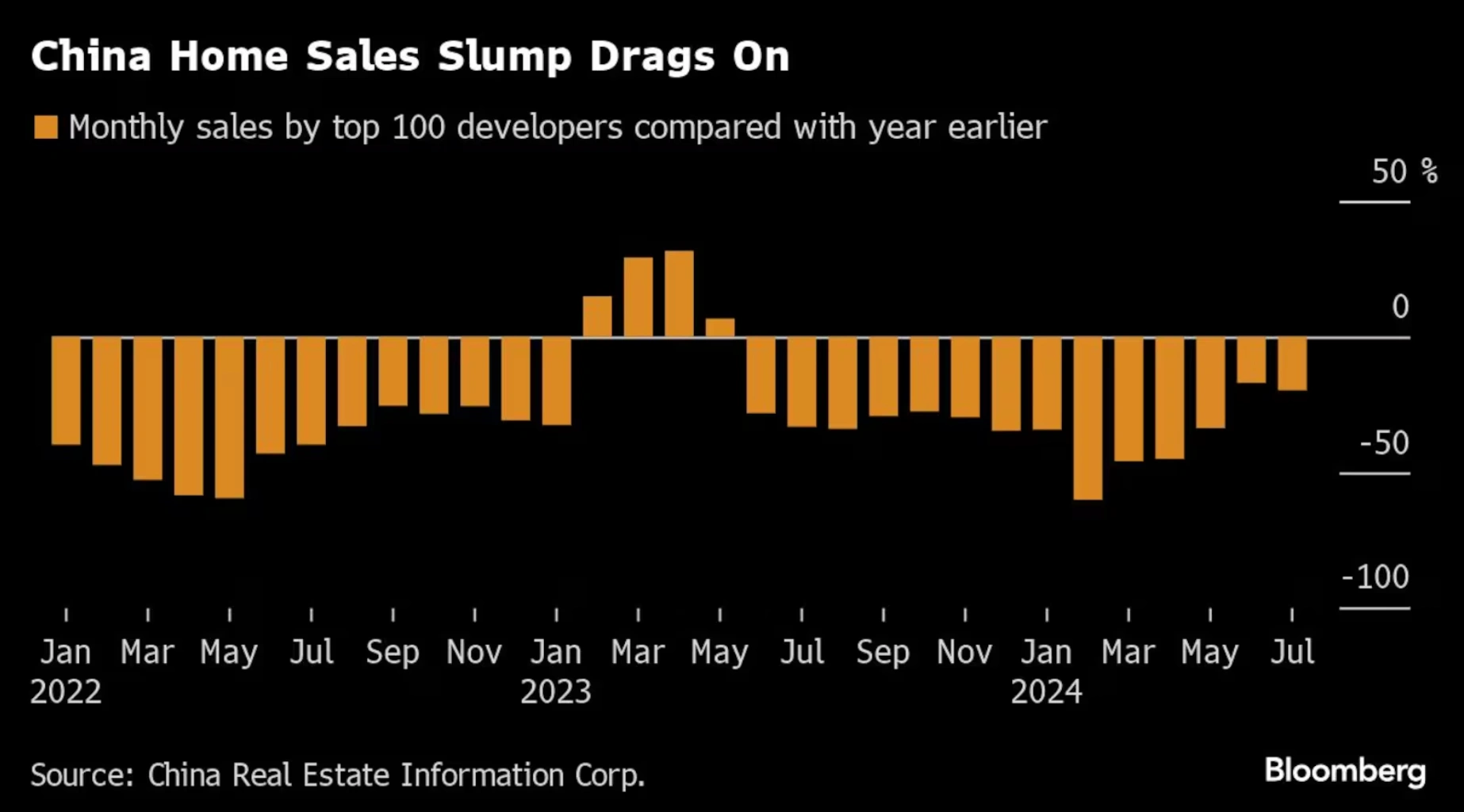

]]>After more than twenty years of development, China’s real estate market has undergone major “adjustments” in the past four years—from 2021 to 2024.

If you look at annual indicators on a month-over-month or year-over-year basis, it’s hard to see how much it has actually declined. You need to compare last year’s metrics with those of 2020 to understand the magnitude of the decline over the four years.

When discussing real estate, five indicators are typically mentioned.

The first indicator is the total construction volume of real estate, including residential and non-residential properties. In 2020, it was 2.2 billion square meters, while the total data for 2024 is not yet available but based on the data from the first eleven months and estimating one more month, it is over 600 million square meters.

From 2.2 billion to over 600 million is a drop of more than 60%, nearly 65%. Imagine this—originally 2.2 billion, now 600-700 million; that’s a serious decline.

The second indicator, aside from construction, is the sales of completed homes. In 2020, new home sales were 1.8 billion square meters, while last year’s sales volume was 500 million square meters, which is also a decline of about 60%. That’s two indicators, each down over 60%.

The third indicator is land leasing volume. In 2020, national land leasing amounted to 8.7 trillion yuan, while the estimate for 2024 is around 3 trillion, which is still relatively optimistic. From January to October, the land leasing volume was actually over 2 trillion. Even if the last two months add another trillion, it would just exceed 3 trillion. In summary, 8.7 trillion minus over 5 trillion is about a 30% reduction.

So, three significant indicators have dropped over 60%.

The fourth indicator that everyone is concerned about is housing prices. Overall, housing prices have dropped by 40% to 50%. By the end of 2024, the figures are not yet out, but as of November, the national statistical indicators show housing prices have dropped by 40% compared to 2020. Some places have dropped a bit more and some a bit less, etc.

The fifth indicator is that real estate has historically accounted for 45% of all financing in China’s financial system. Last year, the public’s desire to buy houses significantly decreased, leading to a 50% annual reduction in mortgage loans compared to 2020. Developers want funds, but their credibility is poor and their debt levels are extremely high, so banks are hesitant to lend large amounts to developers. Consequently, developers’ financing abilities have also weakened significantly, with a reduction of about 50%.

In summary, among the five indicators, three have dropped by two-thirds, and two are down nearly 50%. In this sense, you can certainly say that China’s real estate market has undergone a very serious adjustment, the most severe in 20 years.

The real estate sector emerged in the 1990s, and from 2000 to 2010, there was actually no significant adjustment over those twenty years; it was a period of continuous growth and prosperity. So a major adjustment after twenty years is quite normal.

There is now a concern about real estate, with some believing that the extent of China’s adjustment is even more severe than that of Japan.

The second point is whether the crisis in China’s real estate market will trigger a subprime mortgage crisis similar to that in the United States in 2007 and 2008. The so-called subprime mortgage crisis was a crisis brought about by the real estate crisis.

We can clearly state that China’s real estate market does not have the genetic predisposition for a subprime mortgage crisis like that in the U.S., nor does it carry the genes of Japan’s real estate dragging down its economy for twenty years.

What does this mean? We need to explain this concretely.

First, the U.S. subprime mortgage crisis was the result of unprecedented and economically irrational decisions made by the U.S. government after the internet bubble and the 9/11 attacks, which led to economic stagnation.

At that time, the government allowed all Americans to buy homes with zero down payment, meaning no initial capital was required. After purchasing a home, if the price increased by 20%, the loan covered 80% of the value, thus leaving 20% as equity.

The government also allowed people to cash out, borrowing again based on the 20% that had turned into equity. They could use this cash for living expenses, travel, or consumption. This created chaos in the U.S. economy for about seven or eight years.

Because of subprime mortgages, real estate sales went smoothly, and banks were not afraid of going bankrupt. They packaged subprime loans as CDS bonds and issued them in the U.S. capital markets, even leveraging them up to 40 times—meaning with $100 million to buy bonds, one could acquire $4 billion, effectively overdrawing.

In the end, the subprime mortgage crisis hit, Lehman Brothers collapsed, leading to a tsunami that resulted in $10 trillion in bad assets worldwide.

In contrast, the Chinese government has always been clear-headed and has never allowed any local government or enterprise to offer zero down payment for homes. If there were any violations allowing zero down payment, they would be immediately shut down upon discovery.

Second, various bad debts in China’s real estate sector have never been bundled together to issue bonds that would enable high leverage.

In summary, if there are bankruptcies in real estate, they will be the bankruptcies of individual companies. If there are bad debts, they will be localized; there is no multi-fold leverage turning into bad debts in the financial market, nor is there a frenzied high leverage or zero down payment scheme for the public to buy homes, creating numerous bubbles.

Therefore, there is no such financial gene in China.

Even if there are problems in China’s real estate sector now, they are issues of excessive inventory, inventory reduction, and high debt ratios of real estate companies. In short, we should not confuse China’s real estate issues with those of the U.S. or the subprime mortgage crisis, imagining how terrible it could be. This kind of thinking only leads to self-inflicted disarray and exaggeration of the situation.

The second concept is that we should not compare the current real estate adjustments with Japan’s real estate adjustments in the 1990s; these are completely unrelated matters.

Why did Japan’s real estate bubble drag down its economy for 25 to 30 years? It was because the adjustment of Japan’s real estate bubble was combined with the collapse of its financial system. The collapse of the financial system was not driven by the real estate bubble, but was due to the yen itself.

In the 1980s, the yen appreciated twofold, and after 1990, it depreciated twofold. This led to fluctuations of nearly three to four times.

This appreciation and depreciation of the yen were part of the U.S. strategy against Japan. During this process, Japan lacked effective countermeasures and ultimately suffered a major blow from the U.S., resulting in a world-class financial “harvesting.” The destruction of finance, combined with the real estate bubble—when the yen depreciated, it exacerbated the situation.

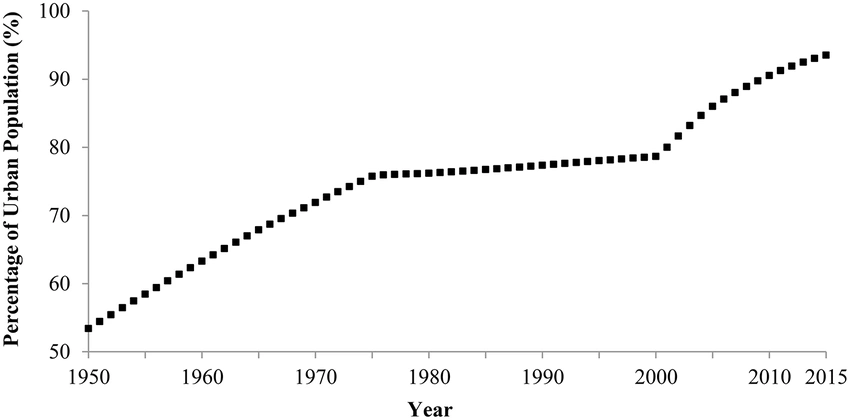

Moreover, at the time of the 1990 real estate bubble collapse, Japan’s urbanization rate had already reached 77%.

This urbanization rate of registered residents has only risen to about 78% or 79% over the past 20 years.

This means that in the 1990s, Japan’s urbanization peaked. After reaching this peak, following the real estate bubble, a large number of houses were left unsold, with no rural population moving to cities to take them up, which led to stagnation.

In contrast, during this real estate adjustment in China, our registered urbanization rate is still only halfway, at 48%. Over the past few decades, it has increased by 30 percentage points, and it can still increase by another 30 percentage points in the coming decades.

Therefore, we have enough room for adjustment and resolution in the future.

In summary, real estate is also a leading industry. When real estate declines, over forty related manufacturing industries—such as machinery, home appliances, and construction—will also suffer. Real estate is also a significant employment sector, and this downturn could lead to the loss of millions of construction jobs.

In short, this issue must be addressed.

China’s urban-rural integration will provide a foundational demand for residential real estate development in the next 20 years. The demand is still there and will gradually be released.

Currently, there are straightforward measures for rescuing the real estate sector. At least since the Third Plenary Session and the September 24 meeting, various departments have laid out at least five measures in the economic work conference documents.

The first measure is that the government initially allocated 300 billion yuan last year, and by the end of September, it clearly announced an allocation of 3 trillion yuan.

I estimate that by next year, there will be another 3 trillion yuan, or even 6 trillion yuan in total. Ultimately, there will be tens of trillions, or even 100 trillion yuan, to acquire the inventory in real estate.

The key issue in this real estate crisis is overcapacity, with approximately 2 billion square meters of unsold new homes. This inventory could lead to a cash flow of over 10 trillion yuan that will not return. If it doesn’t return, real estate companies will face a broken capital chain, leading to various triangular debt issues.

If our country invests tens of trillions, housing prices are currently discounted to about 60% or 70% of their normal prices. At a 60% discount, 1 trillion yuan could buy 1 billion square meters, but now it could buy 1.6 billion square meters, allowing for a significantly greater purchase of homes.

The government can use this concept to buy 1 billion, 1.5 billion, or even 2 billion square meters of inventory, transforming developers’ inventory into state-owned property that can be rented to the public as affordable housing.

Any country should have such public housing. Public housing is for the residents and urban citizens; Hong Kong has 50%, Singapore has 70%, and typical countries have about 20%-25%. Our country has also clearly stated the goal of establishing around 20%-25% of state-owned affordable housing for the public.

Over the past few years, due to the overheating of the real estate market, the government’s affordable housing only accounts for 5% of the total demand.

With a population of 1 billion, if we assume that 200 million people need government-subsidized housing, requiring about 20 billion square meters at 10 square meters per person, and currently, we have only 5%, we need to add another 15-16 percentage points, which means purchasing 10 billion to 20 billion square meters. If the government acquires this 20 billion square meters, it can provide housing for 200 million urban residents—whether migrant workers needing rental housing or recent graduates who cannot afford to buy homes. This would serve as a safeguard.

Meanwhile, developers would receive this money, which would amount to 5 trillion yuan—not as profit, but to repay debts. When 5 trillion yuan reaches creditors, they will repay their debts, creating a cycle that can clear tens of trillions in triangular debts. So, this is a win-win situation that the government is currently promoting.

Finally, is the government stuck in this situation? Will it be trapped with 5 trillion or 10 trillion yuan in debt for decades? Not necessarily.

Because if the government buys homes at a 60% discount and rents them out as public housing, the rental prices for commercial housing would also be about 60% lower. This means that the investment and returns are balanced. The rental income can be used to create REITs and issue ABS (Asset Backed Securities) in the capital market, which can yield around 4% interest income.

The public currently has over 100 trillion yuan in deposits with an interest rate of 1.8%. They would be happy to invest 10 trillion yuan in government bonds to achieve a 4% return.

Thus, this initiative achieves three benefits: It increases the capital available for public investment;It enhances the government’s ability to provide housing for 20% of the population;Developers can sell their unsold inventory accumulated over ten to twenty years to the government at a 60% discount.

This approach allows for debt resolution and is currently in progress.

The second measure is that the government has already allocated several trillion yuan to support local governments in further upgrading dilapidated buildings in urban villages.

It has also been suggested that the 20,000 towns with messy and old buildings should be included in this renovation effort because they are part of the urban landscape. These measures indicate that there are still many infrastructure projects to be undertaken in China over the next three to five years.

This is the second signal to activate the market.

The third point is that after this renovation, the financing of China’s real estate system will be adjusted, aiming to reduce developers’ debt ratios from 80% or 90% down to around 50%.

Real estate is a capital-intensive industry. Worldwide, real estate developers’ debt ratios do not exceed 50%. Even in Hong Kong, the average debt ratio for developers is 30%-40%.

China’s 80% or 90% debt levels are due to borrowing for land, borrowing to develop homes, and borrowing for mortgages before the homes are sold—three layers of debt that accumulate to 80% or 90%. This indicates that we have not managed things well from the outset; we should follow universally accepted rules. The funds for purchasing land should not be 80% or 90% financed by banks; instead, they should rely on equity capital. This is a fundamental principle.

In Chongqing, for instance, developers have relatively lower debt ratios for this reason. You cannot allow excessive debt accumulation, leading to skyrocketing land prices from 3 million to 10 million yuan per mu (approximately 0.165 acres). If this happens, developers may engage in reckless land acquisitions, resulting in the emergence of “land kings,” which must be controlled at the source.

Additionally, the public’s mortgage loans must not allow down payments to be neglected; otherwise, it will lead to financial bubbles and disasters. Therefore, first homes should have a 20%-30% down payment requirement, and second homes should require a 50% down payment, thus balancing the situation.

In summary, the relationship between China’s financial system and the real estate sector will also be resolved during this adjustment.

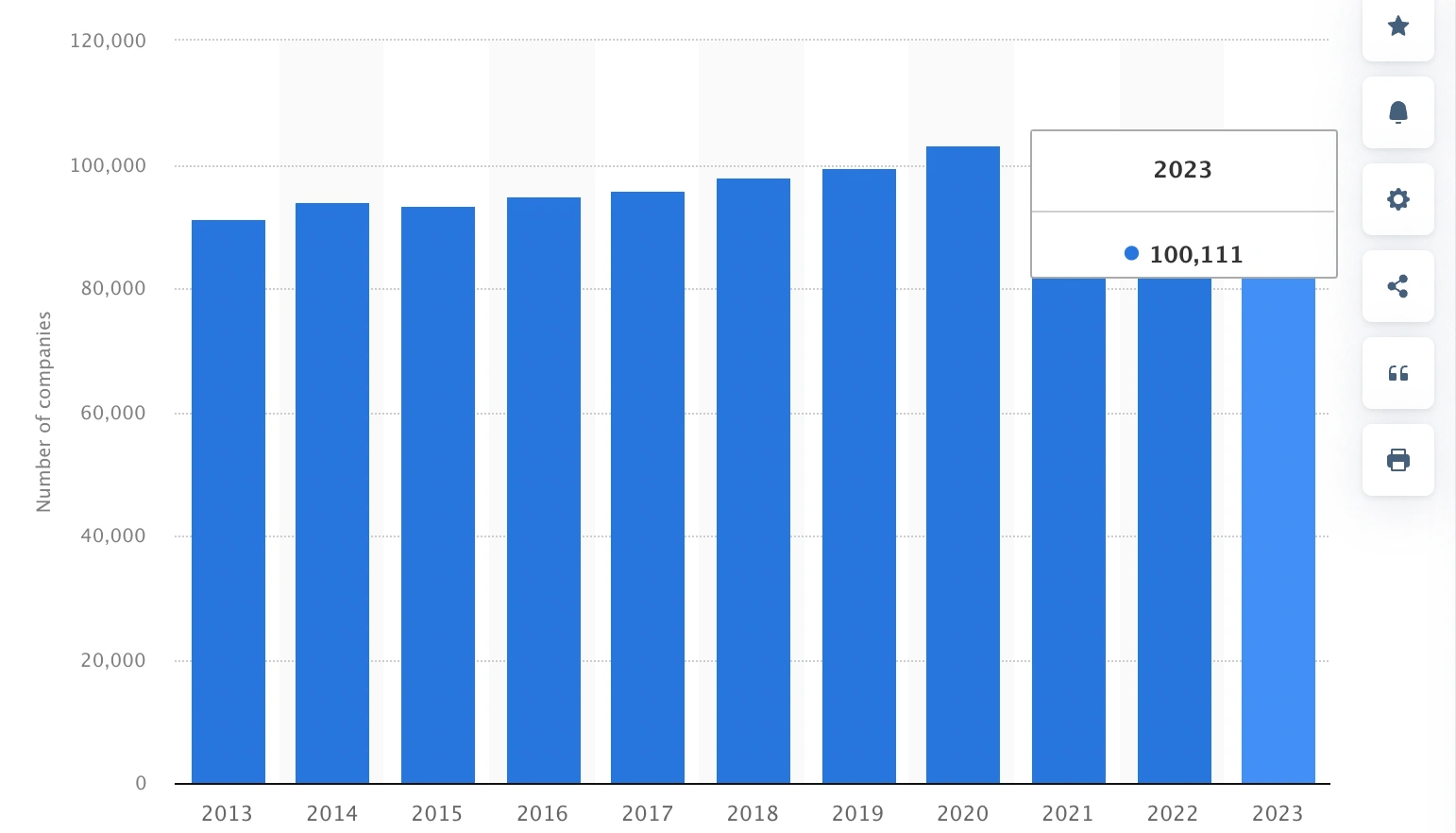

Furthermore, regarding the total number of real estate companies in China, there are currently over 90,000 nationwide. With a population of 1.4 billion and over 900 million urban residents, this means there is roughly one real estate company for every 10,000 people—this is a world record.

In the entire United States, there are fewer than 500 development companies. Even Trump’s family operates a development company. When I spoke with the president of the U.S. Real Estate Association, I specifically asked about this, and he confirmed the number.

In my opinion, within two to three years, if another count is done, the number of registered real estate development companies in China will drop to fewer than 20,000.

Finally, after weathering this storm, China’s real estate sector will enter a new paradigm and a new normal. Whether in finance or construction planning, all aspects will develop better and more orderly.

Finally, the focus is on housing prices.

In China, in 2020, it took 23 to 30 years of household income to buy a home, according to national statistics; globally, it’s generally 7 to 10 years of household income for a family to purchase a home.

With the recent decline, by 2024, housing prices have fallen to the average prices of 2014 and 2015. As a result, the ratio of current housing prices to household income has changed from 20 to 30 years to 10 to 20 years. This reduction in the income ratio is a good thing. If housing prices do not rise again in the next ten years, but GDP doubles every decade and per capita income also doubles, then the ratio of income to housing prices will shrink from the current 10 to 20 years to 8 to 10 years, which is a reasonable cost-performance ratio compared to the world.

In a person’s lifetime, spending one-sixth of their income to buy a home is a common concept in real estate globally. If you don’t buy a home and instead rent, spending one-sixth of your annual income on rent is also reasonable.

If you spend 50% of your annual income on rent, the cost of your housing is too high, and you shouldn’t be renting such a large or expensive place. In the medium to long term, urban-rural integration will provide a large population for cities and absorb a portion of the excess real estate capacity. In the short term, the five measures that have already been introduced are also addressing the real estate challenges.

In summary, by 2025, the decline in China’s real estate market will stabilize, marking the starting point for a new phase of development in the future.

This is a point that should inspire optimism. After 2025, real estate will no longer negatively impact China’s economy as it has in the past four years.

Originally, growth was expected at 7 percentage points, with real estate dragging it down by 2 percentage points, resulting in a final growth of 5 percentage points. At least this year, real estate will no longer have a negative impact; it may not necessarily push positively either, allowing other industries to grow as they should.

Once the decline stabilizes, we do not hope to see housing prices double in the next five years. However, over 15 or 20 years, as GDP doubles, the real estate sector will grow in tandem, creating a new pattern. This is the first part of my discussion today on using reform to address the challenges in real estate.

In the final segment, China should orderly promote the internationalization of the renminbi.

For decades, the internationalization of the renminbi has been cautiously advanced. Now, the report from the 20th National Congress has changed this to “orderly.” The literal meaning is clear: “orderly” implies a stronger push than “cautiously.”

Here, there is a concept: over 40 years of reform and opening up, various economic indicators in China have significantly improved on the world stage. However, the internationalization of the renminbi has remained stagnant, with its global share only around 2%-3% both 40 years ago and now.

There are three categories of currencies in the world. The first category is the U.S. dollar, as the U.S. is a global economic powerhouse, accounting for 25% of global GDP, 50% of trade clearing, and 60% of national foreign exchange reserves. Thus, the U.S. dollar is a strong currency.

The second level includes developed countries, such as the 27 European Union countries, Japan, South Korea, the UK, Canada, etc. Their GDP share corresponds to their currency’s share in the global market. For example, in 1995, Japan’s GDP accounted for 14% of the global total, and the yen accounted for about 13%. Now, Japan’s GDP is only 4% of the global total, with the yen holding a similar 4% share—at least they are proportional.

The third level consists of typical developing countries, which together account for just over 50% of global GDP, but their currencies only represent about 5% of the global currency share. Currently, China’s GDP accounts for 20% of the global total, but our currency represents only 2%-3%, placing us in the same category as typical developing countries. If, in the next 20 years, China becomes an economic powerhouse with GDP reaching 25% or even 30% of the world, will our currency still hold only 2%-3%?

Certainly not.

We won’t claim that we want to replace the dollar or become the world’s dominant currency; that would be unrealistic to discuss at this stage. However, the goal before 2050 should be as stated above. This goal represents a new requirement, thus promoting the internationalization of the renminbi in an orderly manner.

The aforementioned points are my interpretation of the central government’s new tasks regarding openness.

Upon reflection, you will find that the central government’s vision for the next phase of China’s openness embodies a spirit: China’s doors of openness will only continue to widen and will never close.

China is entering a realm of higher-level, deeper, and broader openness.

The post China Will In No Way Repeat U.S. and Japan’s Real Estate Crises first appeared on China Academy.

]]>The post Crisis of China property giant Evergrande: Has China’s Property Bubble Finally Popped? first appeared on China Academy.

]]>Radhika Desai:

let’s do the next topic, which is the property bubble. So, mick, do you want to start us off about the property bubble?

Mick Dunford:

The story started with the housing reform after 1988, when China moved from a welfare system to a commodity system. And then in 1998, it actually privatized down way housing. It took the view that housing should be provided as a commodity by developers. And in 2003 that was confirmed. And from that point on, you saw a very, very substantial growth in the number of developers, many of whom, the vast majority of whom were private developers. So in a sense, they moved to a fundamentally market system. They had to make certain adjustments very quickly because they found that while the quality of housing and the amount of housing space for a person was going up, these developers were targeting their housing to more affluent groups.

There was an underprovision of housing for middle-income groups and for low-income groups. And there was gradually, as you saw over the years, more and more attention paid to the provision of low-cost housing and low-cost rental housing. And in fact, in the current 5-year plan, 25% of all housing is supposed to be basically low-cost housing. The important point is that this problem has arisen in a system that has actually been liberalized in accordance with the recommendations that were made by the World Bank in 1993.

In other words, it is an example of a liberalized, predominantly market, private led system where these difficulties and these problems have merged.

That’s the first thing I want to say. And I obviously to address the housing needs, China has had to move back significantly over time in the direction of providing low-cost housing to meet the housing needs of the Chinese people. But basically, in August 2020, the government became very, very concerned about, on the one hand, rising housing prices and, on the other hand, the explosion of leverage and the fact that the liabilities of many of these developers were substantially exceeding their assets. And the other line on this chart is a line that shows house prices in the United States. Of course, it was the crash, the prices in the subprime market, that in a sense triggered the financial crisis. So China, first of all, is absolutely determined that it should not face the kind of problem that was created by the liberalized housing system in the United States.

So that’s basically the first thing I want to say. I think if you want, I can say something about the case of ever growing. But basically what China did in 2020 was they introduced what they called the three red lines, which were basically designed to reduce financial risks, but it had a number of consequences because it deflated the housing market to some extent. Housing prices started to fall, some of these developers found themselves in a situation where their liabilities significantly exceeded their assets. There was a decline in residential investment. But to some extent I think this is part of a deliberate objective to basically redirect capital towards, as I said, high productivity activities and away from activities, particularly the speculative side of the housing market.

Michael Hudson:

What I’d like to know is the background for this is. How much of this housing is owner occupied? And how much is rental a housing? The other question is how much the ratio of housing costs to personal income? In America it’s over 40 % of personal income for housing. What’s the ratio in China? I’d also want to know the debt equity ratio, how much depth on the average for different income groups, relative to the value of housing.

Radhika Desai:

The blue line, which shows the United States housing prices, you can see that they reached a certain peak in 2008 at 150 times the value of their 2010 values, and then they went down to below the 2010 level. But the U.S. monetary policy, the Federal Reserve policy, it’s the continuation of the regulated financial sector, the easy money policy, which has been applied in a big way with the zero-interest rate policy, with quantitative easing, et cetera, has simply led to a new real estate boom, where real estate prices have reached a peak that is even higher than that of 2007-2008, which was such a disaster.

This was all made possible precisely by increasing housing debt, et cetera. Whereas in China, a big driver of the housing boom was actually people investing their savings in housing. So, logically, it means that the level of debt in the housing market will be comparatively lower. The entities that are in debt are actually the developers. That’s a very different kind of problem than the owners being in debt.

Mick Dunford:

The problem is the indebtedness of the developers and the existence of debts that far exceed the value of their assets.

And the way in which this situation has come about. And as I said, the Chinese government wants to address the financial risks associated with this situation, has done so by introducing these so-called 3 red lines, is also interested in reducing housing prices and is also interested in redirecting finance towards productivity, increasing activities.

So Evergrande is an enormous real estate giant. It has $300 billion in debt. It has $20 billion in overseas debt, and its assets, according to its accounts at the end of the last quarter of last year, were $242 billion. And 90% of those assets are in mainland China. Its debt-asset ratio was 84.7%, and the three red lines set a limit of 70%.

So it’s well above the red line. In 2021, it defaulted. And then in January this year, it was ordered to liquidate after the international creditors and the company failed to agree on a restructuring plan. In September last year, by the way, its chairman, Xu Jiayin, was placed under coercive measures on suspicion of unspecified crimes. Basically, it was a Hong Kong court that called in the liquidators. And the reason was that outside of China, Evergrande looked like a massively profitable distressed debt trading opportunity. There was 19 billion in defaulted offshore bonds with very substantial assets. And initially there was a view that the Chinese government might prop up the real estate market. So a lot of us and European hedge funds basically piled into the debt, expecting quite large payouts. But it seems that these negotiations were to some extent controlled by a risk management committee in Guangdong. And the authorities basically were very, very reluctant to allow offshore claimants to secure onshore income and onshore assets.

In fact, to stop the misuse of funds, I think about ten local Chinese provinces actually took control of the pre-sale revenues. They put it in escrow accounts. And the idea was that this money should basically be prioritized to make sure that the houses of the people who had paid deposits for houses were actually built, and the people who had done the work of building houses were basically paid, and then we saw the value of these offshore bonds collapse very rapidly indeed.

And I think that to some extent explains the concerns of the international financial market about the difficulties of this particular case.

But I think it’s clear that China is basically turning to deflate this sector and to put an end to this speculative real estate market as much as possible and to redirect capital into productivity-enhancing, essentially the industrial sector.

These creditors, bondholders and also other creditors, basically shareholders, are going to take a very big haircut.

Radhika Desai:

Exactly. I think this is the key, that there will be an imposition of haircuts on the rich and powerful, not just subjecting ordinary people to repossession of their home, which they should have access to.

So, as Mick said, the Chinese government is doing everything possible to make sure that the ordinary buyers who bought these houses do not lose out, which is the opposite of what was done in trying to solve the housing and credit bubble in the United States.

The Chinese government is well aware that the whole thing that caused this whole housing bubble is in good part a product of the fact that when relations between China and the West were much better, China accepted some advice from the World Bank. And this is partly a result of that and the kind of deregulation that the World Bank had suggested. But it is very clear now that relations between China and the West are not good. In fact, they are anything but good. China is unlikely to be once bitten twice shy. Even if they were good, and now that they’re not good, they will be.

And China is clear. Looking at distinctively pragmatic, socialistic ways out, and you see in the new, they are addressed to the NPC by the Premier that social housing has become a major priority, not building houses for private ownership, but rather building houses that will be kept in the public sector and rented out at affordable rates. And I think that is a really important thing. Really the way to go. And finally, I would say that the housing bubble in Japan and the housing bubble in the United States were bound to have very different consequences, partly because of two reasons, mainly number one, the nature of the financial systems were very different.

In the case of Japan, the financial system was transformed from one that resembled China’s financial system to one that resembled the U.S. financial system much more. And Japan has continued that transformation and has suffered as a result. I would say, in short, Japan has really been the price of keeping its capital economy capitalist. So, in many ways, so is the United States. The second reason is that, funnily enough, one of the effects of the Plaza Accord was that by the time the Plaza Accord came along, Japan was no longer interested in buying our Treasuries. And as a result, the United States essentially restricted its access to the U.S. markets to a much greater extent. And so Japan essentially lost those export markets, it did not do what China is able to do. It may not have been able to do what China is able to do as a capitalist country, which is to massively redirect the incentives for production away from exports and toward the domestic market, including the investment market.

Mick Dunford:

So I think the japanification course is not one that China will follow, that China will actually address this, need to innovate and transform its industrial system, in order in a sense, address the problems that are associated with the earlier drivers of Chinese development.

The post Crisis of China property giant Evergrande: Has China’s Property Bubble Finally Popped? first appeared on China Academy.

]]>The post If house prices are allowed to fall freely, how much will house prices fall? first appeared on China Academy.

]]>For the national real estate market, the freedom to lower prices for new homes is a very important signal, indicating that housing prices will squeeze out the bubble, and the true level of housing prices will gradually surface.

It is well known that local governments are always very sensitive to the price reduction behavior of developers. Due to concerns that significant price reductions may trigger negative chain reactions and even lead to a collapse of the local real estate market, many local governments do not allow developers to make large price reductions. Even in cities where there is severe oversupply, there are strict regulations on the extent of price reductions, such as not being allowed to be lower than 10%-15% of the recorded price.

However, in the current downward cycle of the real estate market, such price reductions do not reflect the true price level. Many real estate projects need further price reductions to stimulate transactions. Under the local government’s limit order, many developers have to indirectly lower prices, such as offering property management fees or giving away gold with home purchases.

If any developer dares to make significant direct price reductions, it may be classified as a “malicious price reduction.” In May of this year, two real estate developers in Kunshan City, Jiangsu Province, reduced their prices and were penalized by the local Housing and Construction Bureau. The reason given was “unauthorized significant price reductions for sales, disrupting market order, and causing factors of social instability.” The Housing and Construction Bureau also emphasized that local real estate companies should take it as a warning and consciously maintain the order of the real estate market. Violators will be strictly dealt with.

However, although administrative measures can deter individual enterprises, they cannot ultimately stop the overall downward trend of the market. Moreover, distorting normal pricing behavior in the market through administrative will can lead to even greater negative effects.

With the continuous decline of the real estate market, more and more enterprises face enormous cash flow pressures. If developers are not allowed to lower prices for promotional purposes, many developers will face the risk of cash flow disruption and debt default, leading to more and more unfinished real estate projects. This will give rise to social issues that ultimately require government intervention.

In addition, the real estate crisis will also spread to the banking system, potentially triggering a large-scale financial storm. Real estate has always been seen as the gray rhino of the Chinese economy. If developers experience cash flow disruptions due to the inability to lower prices, the gray rhino of the real estate market may become a reality. Only by allowing price reductions for new homes can the current stalemate in the real estate market be broken and prevent the further escalation of the real estate crisis.

As the negative consequences of restricting price reductions become more apparent, the attitude of regulatory authorities is beginning to loosen. In August of this year, the Ministry of Housing and Urban-Rural Development’s official media, “China Real Estate News,” published an article titled “Real Estate Financial Risks Intensify, Expecting Adjustments and Optimizations of Policies to be Implemented as Soon as Possible (Translated).” The article stated, “Developers should be given greater autonomy in pricing, allowing them to engage in self-rescue through price reductions and quickly recoup funds.” The icy restrictions on price reductions are showing signs of melting.

More importantly, restricting price reductions by developers will ultimately impact local governments. Because the real estate industry’s model has always emphasized rapid turnover, if developers cannot quickly sell their inventory of properties, the inventory will continue to accumulate, and developers will lack funds to acquire land and develop new projects. This will greatly impact the fiscal income of local governments.

In 2022, the nationwide land transfer fees decreased significantly by 30%. This year, the land market continued to cool down, and the land transfer revenue in the first three quarters decreased by another 20% compared to the low base of the previous year. In some places, the decline even exceeded 40%. The consequences of unsold houses have finally affected local governments, causing pain for some local governments that heavily rely on land finances.

In this context, many local governments have to make a choice: whether to maintain housing prices or prioritize land revenue. Different local governments are showing divergence in their approaches.

Some local governments choose to continue to maintain housing prices. At the end of November, a real estate project in Chengdu reduced prices by 40%, which was characterized by the local management committee as “suspected of disrupting the normal order of the real estate market” and its record was temporarily suspended. However, more local governments have started to relax regulations on price reductions. In August of this year, a real estate project in Zhuhai conducted a half-price promotion, and the local Housing and Construction Bureau stated that “the price reduction approach taken by the project is a reasonable market behavior” and allowed the price reduction.

Suzhou’s lifting of price restrictions on developers sends an important signal to the national real estate market. With its GDP ranking 6th in the country, even Suzhou, with its economic strength, has started to prioritize land revenue over housing prices. This indicates that many other local governments are likely to face the same choice, and it is expected that more local governments will lean towards prioritizing land revenue.

As more and more local governments begin to lift restrictions on price reductions for new homes, it will have a significant impact on the national real estate market. The current domestic real estate market is largely in a stalemate because prices have not fallen sufficiently, resulting in a rapid decline in transaction volume. The reason prices have not fallen sufficiently is directly related to the restrictions on price reductions for new homes.

In the new home market, the pricing of new homes is highly influenced by administrative power, deviating significantly from the true market price. Even the seemingly market-based pricing of second-hand homes is inevitably affected by the pricing of new homes because if new home prices do not decrease, it largely supports the pricing of second-hand homes. The limited decrease in second-hand home prices in many cities is mainly because many sellers of second-hand homes currently do not have financial pressure and are unwilling to significantly reduce prices proactively.

However, once restrictions on price reductions for new homes are lifted, housing prices in the country will face a reprice shock. Many developers are under significant debt pressure, and they will increasingly choose to reduce prices significantly to recover funds. If they do not reduce prices significantly, many developers will face the risk of bankruptcy.

If new homes experience significant price reductions, it will eventually impact the second-hand home market as well. If second-hand home prices remain high, the limited number of buyers will flow into the new home market. Even sellers of second-hand homes who are not in dire need of money will have to reduce prices proactively under the pressure of price reductions in the new home market.

The post If house prices are allowed to fall freely, how much will house prices fall? first appeared on China Academy.

]]>